Taxes can have a big impact on your total investment returns. And with tax season here, it’s a great opportunity to revisit your investment portfolio and how tax-deferred and tax-free investments fit into your overall strategy. When making investment decisions, be sure to look for ways to help maximize tax benefits in addition to other considerations like potential risks, the expected rate of return and the quality of an investment.

The difference between taxable, tax-deferred and after-tax savings accounts

With taxable accounts, such as savings accounts, certificates of deposit (CDs) and investment accounts with a brokerage firm, the money you contribute to these accounts has already been taxed once. You then have to pay taxes on any interest and investment earnings on these accounts each year.

Tax-deferred savings accounts include traditional 401(k) or IRA accounts. Tax deferral is the process of delaying (but not necessarily eliminating) until a future year the payment of income taxes on income you earn in the current year. For example, the money you put into your traditional 401(k) retirement account isn’t taxed until you withdraw it, which might be 30 or 40 years down the road!

Tax deferral can be beneficial because:

- The money you would have spent on taxes remains invested

- You may be in a lower tax bracket than you are now when you make withdrawals from the account (for example, when you’re retired)

- You can accumulate more dollars in your accounts due to compounding

Compounding means that your earnings become part of your underlying investment, and they in turn earn interest. In the early years of an investment, the benefit of compounding may not be that significant. But as the years go by, the long-term boost to your total return can be dramatic.

After-tax retirement accounts – Roth 401(k) and IRAs, for example – are those in which you contribute after-tax money, allowing you to avoid paying taxes later during retirement. The money in these accounts grow over time and can be taken out tax-free, as long as you meet certain requirements.1

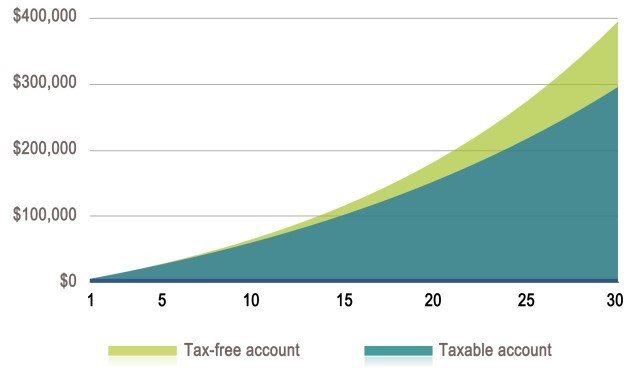

Taxes can make a big difference in your earnings

Let’s assume two people have $5,000 to invest every year for a period of 30 years. One person invests in a tax-free account like a Roth 401(k) that earns 6% per year, and the other person invests in a taxable account that also earns 6% each year. Assuming a tax rate of 28%, in 30 years the tax-free account will be worth $395,291, while the taxable account will be worth $295,896. That’s a difference of $99,395.2

Tax-advantaged savings accounts for retirement

One of the best ways to accumulate funds for retirement or any other investment objective is to use tax-advantaged (i.e., tax-deferred or tax-free) savings accounts, when appropriate. Here are some to consider:

- Traditional IRAs — Anyone under age 70½ who earns income or is married to someone with earned income can contribute to an IRA. Depending upon your income and whether you’re covered by an employer-sponsored retirement plan, you may or may not be able to deduct your contributions to a traditional IRA, but your contributions always grow tax deferred. However, you’ll owe income taxes when you make a withdrawal.1 You can contribute up to $6,000 (for 2019) to an IRA, and individuals age 50 and older can contribute an additional $500 (for 2021).

- Roth IRAs — Roth IRAs are open only to individuals with incomes below certain limits. Your contributions are made with after-tax dollars but will grow tax deferred, and qualified distributions will be tax free when you withdraw them. The amount you can contribute is the same as for traditional IRAs. Total combined contributions to Roth and traditional IRAs can’t exceed $6,000 (for 2021) for individuals under age 50.

- SIMPLE IRAs and SIMPLE 401(k)s — Savings Incentive Match Plan for Employees (SIMPLE) plans are generally associated with small businesses. As with traditional IRAs, your contributions grow tax deferred, but you’ll owe income taxes when you make a withdrawal.1 You can contribute up to $13,500 (for 2021) to one of these plans; individuals age 50 and older can contribute an additional $3,000 (for 2019). (SIMPLE 401(k) plans can also allow Roth contributions.)

- Employer-sponsored plans (401(k)s, 403(b)s, 457 plans) — Contributions to these types of plans grow tax deferred, but you’ll owe income taxes when you make a withdrawal.1 You can contribute up to $19,500 (for 2021) to one of these plans; individuals age 50 and older can contribute an additional $6,500 (for 2021). Employers can generally allow employees to make after-tax Roth contributions, in which case qualifying distributions will be tax free.

- Annuities — You pay money to an annuity issuer (an insurance company), and the issuer promises to pay principal and earnings back to you or your named beneficiary in the future (you’ll be subject to fees and expenses that you’ll need to understand and consider). Annuities generally allow you to elect to receive an income stream for life (subject to the claims-paying ability of the issuer). There’s no limit to how much you can invest, and your contributions grow tax deferred. However, you’ll owe income taxes on the earnings when you start receiving distributions.1

Tax-advantaged savings accounts for college3

For college, tax-advantaged savings accounts include:

- 529 plans — College savings plans and prepaid tuition plans let you set aside money for college that will grow tax-deferred and be tax-free at withdrawal at the federal level if the funds are used for qualified education expenses. These plans are open to anyone regardless of income level. Contribution limits are high–typically over $300,000–but vary by plan.

- Coverdell education savings accounts – Coverdell accounts are open only to individuals with incomes below certain limits, but if you qualify, you can contribute up to $2,000 per year, per beneficiary. Your contributions will grow tax-deferred and be tax-free at withdrawal at the federal level if the funds are used for qualified education expenses.

- Series EE bonds — The interest earned on Series EE savings bonds grows tax-deferred. But if you meet income limits (and a few other requirements) at the time you redeem the bonds for college, the interest will be free from federal income tax too (it’s always exempt from state tax).

Bottom line

Tax-advantaged accounts can keep more money in your own pocket and less in Uncle Sam’s. And while tax considerations shouldn’t be your only concern when it comes to investing, it’s worth considering when planning out your investments.

For more information about maximizing your tax benefits with your investments set up a no-obligation appointment with one of our CFS* Financial Advisors at Elevations Credit Union by calling 303-443-4672 x2240.

1 In order to withdraw funds from a Roth account tax-free, funds must be held in the account for at least five years and withdrawn after age 59 ½. Withdrawals prior to age 59 ½ may be subject to a 10% federal income tax penalty unless an exception applies.

2 This hypothetical example is for illustrative purposes only, and its results are not representative of any specific investment or mix of investments. Actual results will vary. The taxable account balance assumes that earnings are taxed as ordinary income and does not reflect possible lower maximum tax rates on capital gains and dividends, as well as the tax treatment of investment losses, which would make the taxable investment return more favorable, thereby reducing the difference in performance between the accounts shown. Investment fees and expenses have not been deducted. If they had been, the results would have been lower. You should consider your personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision as these may further impact the results of the comparison. This illustration assumes a fixed annual rate of return; the rate of return on your actual investment portfolio will be different, and will vary over time, according to actual market performance. This is particularly true for long-term investments. It is important to note that investments offering the potential for higher rates of return also involve a higher degree of risk to principal.

3 Note: Investors should consider the investment objectives, risks, charges, and expenses associated with 529 plans. More information about specific 529 plans is available in each issuer’s official statement, which should be read carefully before investing. Also, before investing consider whether your state offers a 529 plan that provides residents with favorable state tax benefits. The availability of tax and other benefits may be conditioned on meeting certain requirements.

Part of this content has been contributed by Broadridge Investor Communication Solutions, Inc. Copyright 2016.

You know how important it is to plan for your retirement, but where do you begin? One of your first Read more

This tax season, small businesses all around Colorado are looking for ways to reduce their taxes.