As we near the end of the year, many people start to think about whether it makes sense to retire now or keep their career going. There are quite a few considerations to make. One of the most important things to do is to sit down with your financial advisor and make certain that your plan is in place. Our CFS* Financial Advisors at Elevations Credit Union can help you with that! In the meantime, below is some great information from our partners at Broadridge that discusses many of the critical elements that should go into your decision.

Deciding when to retire may not be one decision but a series of decisions and calculations. For example, you’ll need to estimate not only your anticipated expenses, but also what sources of retirement income you’ll have and how long you’ll need your retirement savings to last. You’ll need to take into account your life expectancy and health as well as when you want to start receiving Social Security or pension benefits, and when you’ll start to tap your retirement savings.

Each of these factors may affect the others as part of an overall retirement income plan.

Thinking about early retirement?

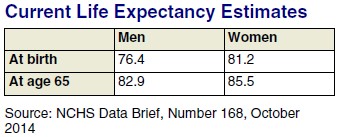

Retiring early means fewer earning years and less accumulated savings. Also, the earlier you retire, the more years you’ll need your retirement savings to produce income. And your retirement could last quite a while. According to a National Vital Statistics Report, people today can expect to live more than 30 years longer than they did a century ago.

Not only will you need your retirement savings to last longer, but inflation will have more time to eat away at your purchasing power. If inflation is 3% a year—its historical average since 1914—it will cut the purchasing power of a fixed annual income in half in roughly 23 years. Factoring inflation into the retirement equation, you’ll probably need your retirement income to increase each year just to cover the same expenses. Be sure to take this into account when considering how long you expect (or can afford) to be in retirement.

There are other considerations as well. For example, if you expect to receive pension payments, early retirement may adversely affect them. Why? Because the greatest accrual of benefits generally occurs during your final years of employment, when your earning power is presumably highest. Early retirement could reduce your monthly benefits. It will affect your Social Security benefits too.

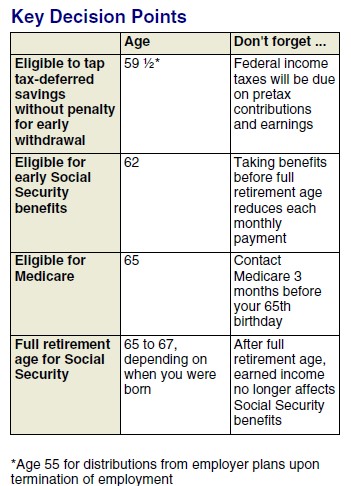

Also, don’t forget that if you hope to retire before you turn 59½ and plan to start using your 401(k) or IRA savings right away, you’ll generally pay a 10% early withdrawal penalty plus any regular income tax due (with some exceptions, including disability payments and distributions from employer plans such as 401(k)s after you reach age 55 and terminate employment).

Finally, you’re not eligible for Medicare until you turn 65. Unless you’ll be eligible for retiree health benefits through your employer or take a job that offers health insurance, you’ll need to calculate the cost of paying for insurance or health care out-of-pocket, at least until you can receive Medicare coverage.

Delaying retirement

Postponing retirement lets you continue to add to your retirement savings. That’s especially advantageous if you’re saving in tax-deferred accounts, and if you’re receiving employer contributions. For example, if you retire at age 65 instead of age 55, and manage to save an additional $20,000 per year at an 8% rate of return during that time, you can add an extra $312,909 to your retirement fund. (This is a hypothetical example and is not intended to reflect the actual performance of any specific investment.)

Even if you’re no longer adding to your retirement savings, delaying retirement postpones the date that you’ll need to start withdrawing from them. That could enhance your nest egg’s ability to last throughout your lifetime.

Postponing full retirement also gives you more transition time. If you hope to trade a full-time job for running your own small business or launching a new career after you “retire,” you might be able to lay the groundwork for a new life by taking classes at night or trying out your new role part-time. Testing your plans while you’re still employed can help you anticipate the challenges of your post-retirement role. Doing a reality check before relying on a new endeavor for retirement income can help you see how much income you can realistically expect from it. Also, you’ll learn whether it’s something you really want to do before you spend what might be a significant portion of your retirement savings on it.

Phased retirement: the best of both worlds

Some employers have begun to offer phased retirement programs, which allow you to receive all or part of your pension benefit once you’ve reached retirement age, while you continue to work part-time for the same employer.

Phased retirement programs are getting more attention as the baby boomer generation ages. In the past, pension law for private sector employers encouraged workers to retire early. Traditional pension plans generally weren’t allowed to pay benefits until an employee either stopped working completely or reached the plan’s normal retirement age (typically age 65). This frequently encouraged employees who wanted a reduced workload but hadn’t yet reached normal retirement age to take early retirement and go to work elsewhere (often for a competitor), allowing them to collect both a pension from the prior employer and a salary from the new employer.

However, pension plans now are allowed to pay benefits when an employee reaches age 62, even if the employee is still working and hasn’t yet reached the plan’s normal retirement age. Phased retirement can benefit both prospective retirees, who can enjoy a more flexible work schedule and a smoother transition into full retirement; and employers, who are able to retain an experienced worker. Employers aren’t required to offer a phased retirement program, but if yours does, it’s worth at least a review to see how it might affect your plans.

Check your assumptions

The sooner you start to plan the timing of your retirement, the more time you’ll have to make adjustments that can help ensure those years are everything you hope for. If you’ve already made some tentative assumptions or choices, you may need to revisit them, especially if you’re considering taking retirement in stages. And as you move into retirement, you’ll want to monitor your retirement income plan to ensure that your initial assumptions are still valid, that new laws and regulations haven’t affected your situation, and that your savings and investments are performing as you need them to.

Interested in learning more? Meet with one of our CFS* Financial Advisors at Elevations Credit Union.

Non-deposit investment products and services are offered through CUSO Financial Services, L.P. (“CFS”), a registered broker-dealer (Member FINRA/SIPC) and SEC Registered Investment Advisor. Products offered through CFS: are not NCUA/NCUSIF or otherwise federally insured, are not guarantees or obligations of the credit union, and may involve investment risk including possible loss of principal. Investment Representatives are registered through CFS. The credit union has contracted with CFS to make non-deposit investment products and services available to credit union members. For specific tax advice please consult a qualified tax professional.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2016.

When you're considering applying for a loan, understand how underwriters look at you and calculate your debt-to-income ratio (DTI), plus Read more

As we look back at the 2015 mortgage market in Colorado’s Front Range, three trends are likely to continue this Read more