How much are you saving for retirement? It’s essential to know how much you can contribute to your IRA, Roth IRA and employer retirement plans. Limits can change year to year. Read on to see what’s changed in 2020.

The maximum amount you can contribute to a traditional IRA or a Roth IRA in 2020 is $6,000 (or 100% of your earned income, if less), unchanged from 2019. The maximum catch-up contribution for those age 50 or older remains at $1,000. You can contribute to both a traditional IRA and a Roth IRA in 2020, but your total contributions can’t exceed these annual limits.

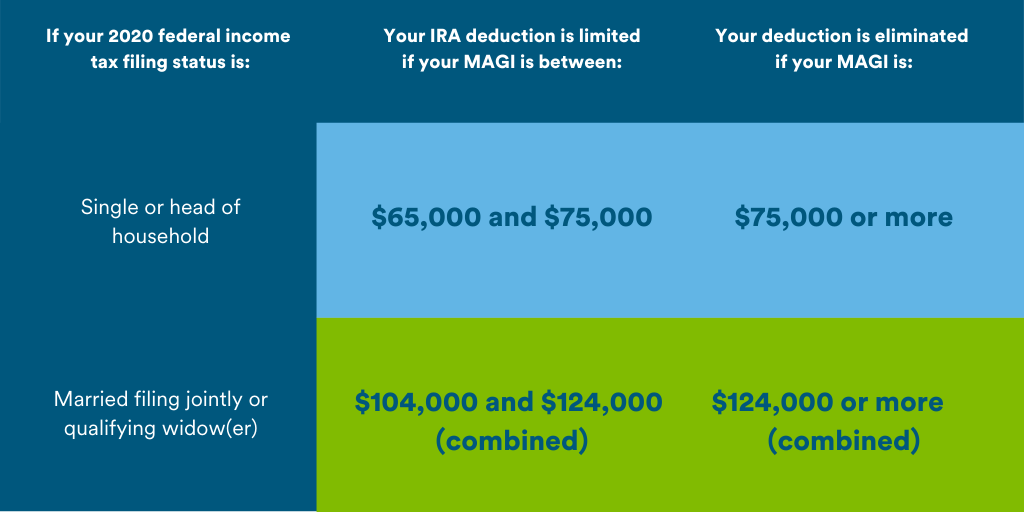

Traditional IRA income limits

If your employer doesn’t offer a retirement plan, your contributions to a traditional IRA are generally entirely tax-deductible. For those who are covered by an employer plan, the income limits for determining the deductibility of traditional IRA contributions in 2020 have increased:

If your filing status is single or head of household, you can fully deduct your IRA contribution up to $6,000 ($7,000 if you are age 50 or older) if your modified adjusted gross income (MAGI) is $65,000 or less (up from $64,000 in 2019). If you’re married and filing a joint return, you can fully deduct up to $6,000 ($7,000 if you are age 50 or older) if your MAGI is $104,000 or less (up from $103,000 in 2019).

If you’re not covered by an employer plan but your spouse is, and you file a joint return, your deduction is limited if your MAGI is $196,000 to $206,000 (up from $193,000 to $203,000 in 2019), and eliminated if your MAGI exceeds $206,000 (up from $203,000 in 2019).

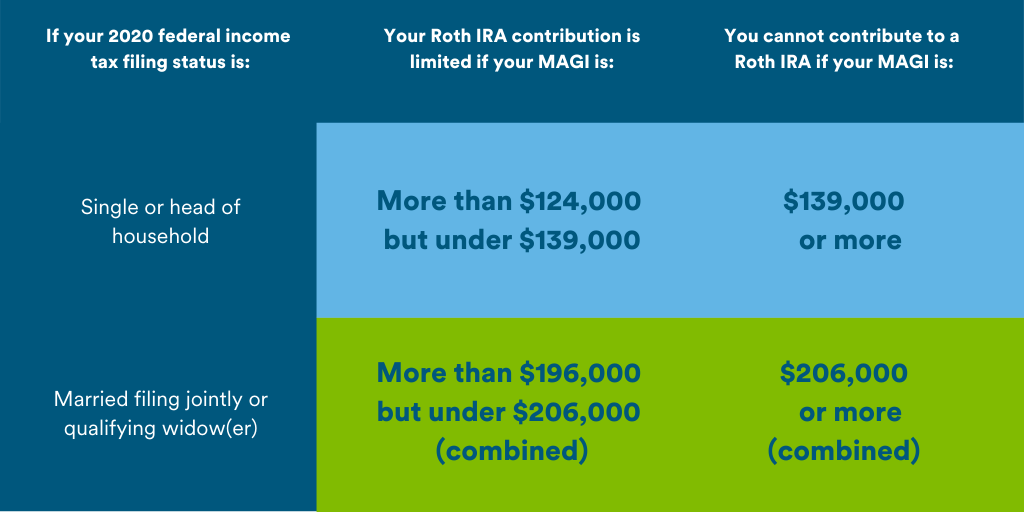

Roth IRA income limits

The income limits for determining how much you can contribute to a Roth IRA have also increased for 2020. If your filing status is single or head of household, you can contribute the full $6,000 ($7,000 if you are age 50 or older) to a Roth IRA if your MAGI is $124,000 or less (up from $122,000 in 2019). And if you’re married and filing a joint return, you can make a full contribution if your MAGI is $196,000 or less (up from $193,000 in 2019). Again, contributions can’t exceed 100% of your earned income.

Employer retirement plans

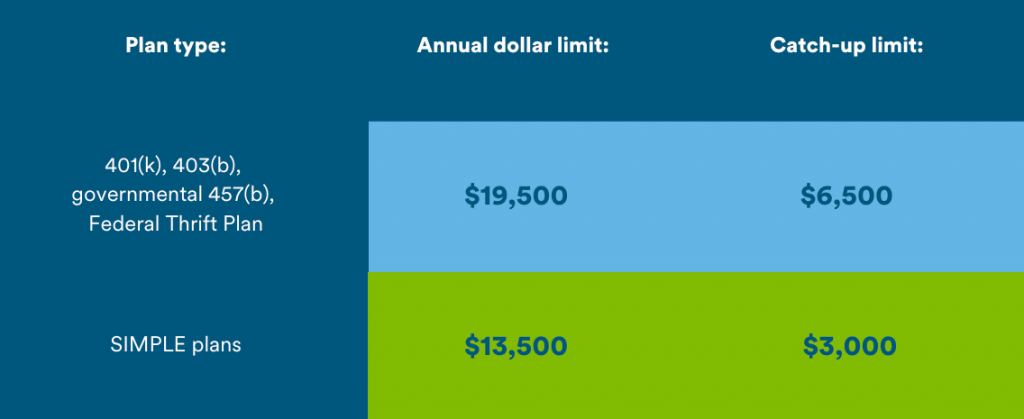

Most of the significant employer retirement plan limits for 2020 have also increased. The maximum amount you can contribute (your “elective deferrals”) to a 401(k) plan is $19,500 in 2020 (up from $19,000 in 2019). This limit also applies to 403(b) and 457(b) plans, as well as the Federal Thrift Plan. If you’re age 50 or older, you can also make catch-up contributions of up to $6,500 to these plans in 2020 (up from $6,000 in 2019). (Special catch-up limits apply to certain participants in 403(b) and 457(b) plans.)

If you participate in more than one retirement plan, your total elective deferrals can’t exceed the annual limit ($19,500 in 2020 plus any applicable catch-up contributions). Deferrals to 401(k) plans, 403(b) plans and SIMPLE plans are included in this aggregate limit, but deferrals to Section 457(b) plans are not. For example, if you participate in both a 403(b) plan and a 457(b) plan, you can defer the full dollar limit to each plan — a total of $39,000 in 2020 (plus any catch-up contributions).

The amount you can contribute to a SIMPLE IRA or SIMPLE 401(k) is $13,500 in 2020 (up from $13,000 in 2019), and the catch-up limit for those age 50 or older remains at $3,000.

Note: Contributions can’t exceed 100% of your income.

The maximum amount that you can allocate to your account in a defined contribution plan (for example, a 401(k) plan or profit-sharing plan) in 2020 is $57,000 (up from $56,000 in 2019) plus age 50 catch-up contributions. (This includes both your contributions and your employer’s contributions. Special rules apply if your employer sponsors more than one retirement plan.)

Finally, the maximum amount of compensation that can be taken into account to determine benefits for most plans in 2020 is $285,000 (up from $280,000 in 2019), and the dollar threshold for determining highly compensated employees (when 2020 is the look-back year) is $130,000 (up from $125,000 when 2019 is the look-back year).

If you have questions about how these limits affect you and your retirement planning, contact a CFS* Wealth Management Advisor today. Please give us a call at 303.443.4672 x2240 to set up a no-obligation appointment to discuss your options further.

*Non-deposit investment products and services are offered through CUSO Financial Services, L.P. (“CFS”), a registered broker-dealer (Member FINRA/SIPC) and SEC Registered Investment Advisor. Products offered through CFS: are not NCUA/NCUSIF or otherwise federally insured, are not guarantees or obligations of the credit union, and may involve investment risk including possible loss of principal. Investment Representatives are registered through CFS. Elevations Credit Union has contracted with CFS to make non-deposit investment products and services available to credit union members.

CUSO Financial Services, L.P. (CFS) does not provide tax or legal advice. For such guidance, please consult your tax and/or legal advisor.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2020.

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

When you're considering applying for a loan, understand how underwriters look at you and calculate your debt-to-income ratio (DTI), plus Read more

In addition to looking at your debt-to-income ratio and credit report, there are several other considerations underwriters take into account Read more